The $1000 Comment

Five years ago, in response to what she perceived as criticism from Serj Tankian at the Genocide Centennial public concert in Republic Square, then-Diaspora Minister Hranush Hakobyan snapped back, saying that diasporans should open bank accounts in Armenia and deposit $1000 each.

She was raked over the coals for this comment, as it fed into the narrative that the Armenian government of the time viewed the diaspora as a cash cow and the main job of the Diaspora Minister was to milk it. The story persisted over a month later, as she continued to defend her proposal. It seems she never understood that the blowback was not about whether Armenian banks offered competitive interest rates; it was due to the harsh, lecturing tone of her delivery, insinuating that the diaspora was not doing enough to support Armenia (and that this absolved the government’s responsibility for the country’s challenges).

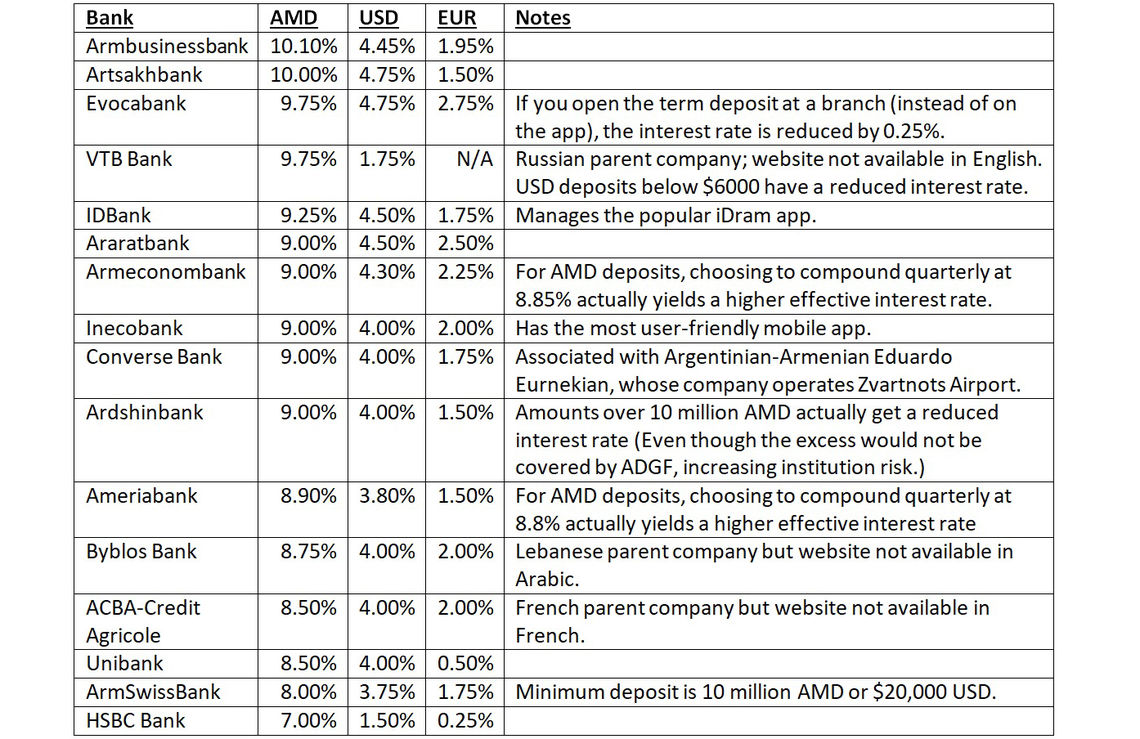

It was 2015 and I had already planned to visit Armenia that summer. I lived in Canada but it would be my fifth trip to the homeland in ten years. In preparation, looking at the websites of a few Armenian banks, I noticed that a one year term deposit in Armenian drams (AMD) could return 10% to 12% in interest. In contrast, my Canadian online savings bank was only offering 1.05% at the time.

So, I brought an extra sum with me on that three week trip. From their websites, I had taken note that Artsakhbank offered the highest interest rate, at 14% for a one-year term deposit, and a possibility to pay taxes to Artsakh at a lower rate. I walked into an Artsakhbank branch in Yerevan and asked if I could open an account. The teller was very confused. “What do you mean you want to open an account?” I was speaking Eastern Armenian and using the standard word for account, hashiv. The fact that he seemed not to know what I was talking about was not reassuring and I still remember the interaction five years later. After some back and forth, I was able to explain that I was eventually interested in leaving a term deposit (avand, in Armenian) but first I wanted to open a regular account, which, in my experience, is the first step in doing business with any North American bank. Instead of discussing checking accounts, he handed me two stapled black-and-white photocopies of their interest rates for different term lengths and currencies. It was clear it was prepared in Microsoft Word. I left the branch without becoming a customer.

I had just taken for granted that I would be able to maintain my account through the bank’s website after I returned to Canada. I had grown up with Internet banking. Even back when I still had a paper route, I would sign on to the Internet with a dial-up modem to tuck away my meagre savings with ING Direct, an online high-interest savings bank. Artsakhbank did not offer such an option at the time (though it seems they do now). Unless I happened to be back in Armenia when the term deposit matured, it was unclear how I could renew it. They didn’t explain to me that I could have set it to auto-renew but still withdrawn prematurely if I didn’t want to wait till the end of the second term. If I would need to incur long-distance telephone charges just to talk to them, it would defeat the whole purpose of chasing a higher interest rate.

From the general dimly-lit atmosphere and my short interaction in that branch, I started (hopefully irrationally) to develop a nagging feeling that I could return in-person a year later with my paper documents in hand and they would just tell me my money is gone due to some small-print technical reason; having heard tales of corruption and sensing a lack of “corporate” business culture, I didn’t have trust in the judicial system to protect my property if I encountered shenanigans.

I did also visit HSBC and ACBA-Credit Agricole that summer, thinking that being associated with foreign banks might make them more reliable. HSBC had the highest fees, widest exchange rate spread and lowest interest rate offered to savers. They did not explain to me whether there was a way to have the monthly account fee waived. I had virtually never paid a bank fee in my life and was not about to start. ACBA-Credit Agricole did have a primitive Internet banking solution available that required me to pay for a physical token, needed to log in. Even at ten times the interest rate I was receiving in Canada, the hassle was just not worth it and I flew back with my cash in my pocket.

Higher Return Means Higher Risk

In hindsight, a five year term deposit from 2015 would have matured this summer, nearly doubling my $1000 to $1925, if I had secured a 14% rate that compounded annually. The same $1000 would only grow to $1100 after five years if invested at 2%, in Canada for example.

It is important to note that those two figures cannot be directly compared, however. Although it turned out that Artsakhbank still exists and the AMD exchange rate to the USD is essentially the same as it was five years ago, there was no guarantee in 2015 that those two assumptions would hold water.

In general, if an investment promises to return a higher percentage, you should expect a lower probability that that promise will be kept. Inversely, purchasing a bond from the U.S. Treasury will have a lower interest rate than one issued by an airline company. The reason is that you can be much more confident the U.S. Treasury will pay your money back when the bond matures, while the airline might have gone bankrupt in the meantime, taking your principal down with it.

The additional risk of taking a term deposit in an Armenian bank, compared to my Canada-based savings bank can be broken down into two separate components: currency risk and institution risk.

Currency risk derives from the fact that exchange rates are not set in stone; when it comes time to convert your money back, you may find that it is no longer worth as much, especially if the country experienced a period of conflict. Those whose savings were in Lebanese or Syrian pounds are painfully too familiar with what can go wrong.

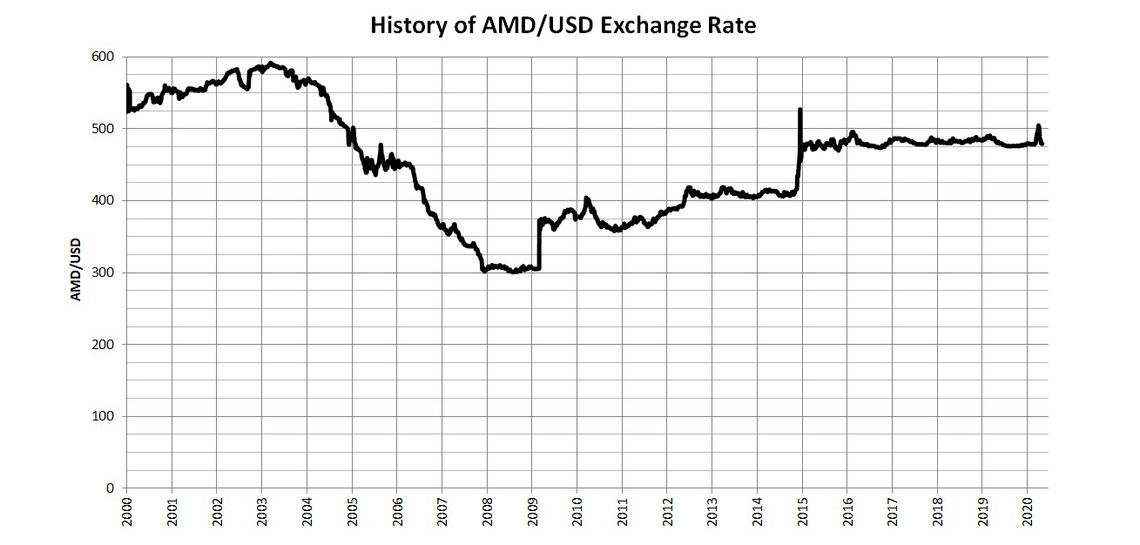

Currency risk can go both ways, however. The currency can also appreciate in value and add to gains. Between 2004 and 2008, the Armenian dram gained 83% against the USD, from an exchange rate of 550:1 to as low as 300:1. (As the number gets smaller, each Armenian dram increases in value.) Even if you kept AMD bills under your mattress, earning zero interest, you would have made a very respectable gain.

That trend proved to be unsustainable, however, once the 2007-2009 global financial crisis began to unfold. After a period of spending foreign currency reserves to keep the exchange rate stable, the Central Bank of Armenia (CBA) allowed its value to fall from 306:1 to 372:1 against the USD on March 4, 2009, as it sought assistance from the International Monetary Fund (IMF). Overnight, the currency had lost 18% of its value. Even if you were earning 12% interest on an AMD-denominated term deposit, you would not be happy. A similar devaluation happened more gradually in December 2014, when a drop in the global oil price took the AMD from 435:1 to 475:1 over the course of the month, a more palatable 8% loss. The currency has remained stable in the 475 range to this day, having now recovered after a short blip over 500 in late March and early April 2020, due to a combination of coronavirus uncertainty and oil shock after-effects. Prime Minister Nikol Pashinyan recently advertised on a Facebook post that the Central Bank had beefed up its foreign currency reserves to help ride out the storm.

EVN Report welcomes comments that contribute to a healthy discussion and spur an informed debate. All comments will be moderated, thereby any post that includes hate speech, profanity or personal attacks will not be published.